Insights for regional businesses

Financial guidance for growing QLD businesses

Practical updates, explanations and insights to help you navigate changing regulations, manage cashflow and strengthen your long-term position

Featured

Browse the Blog

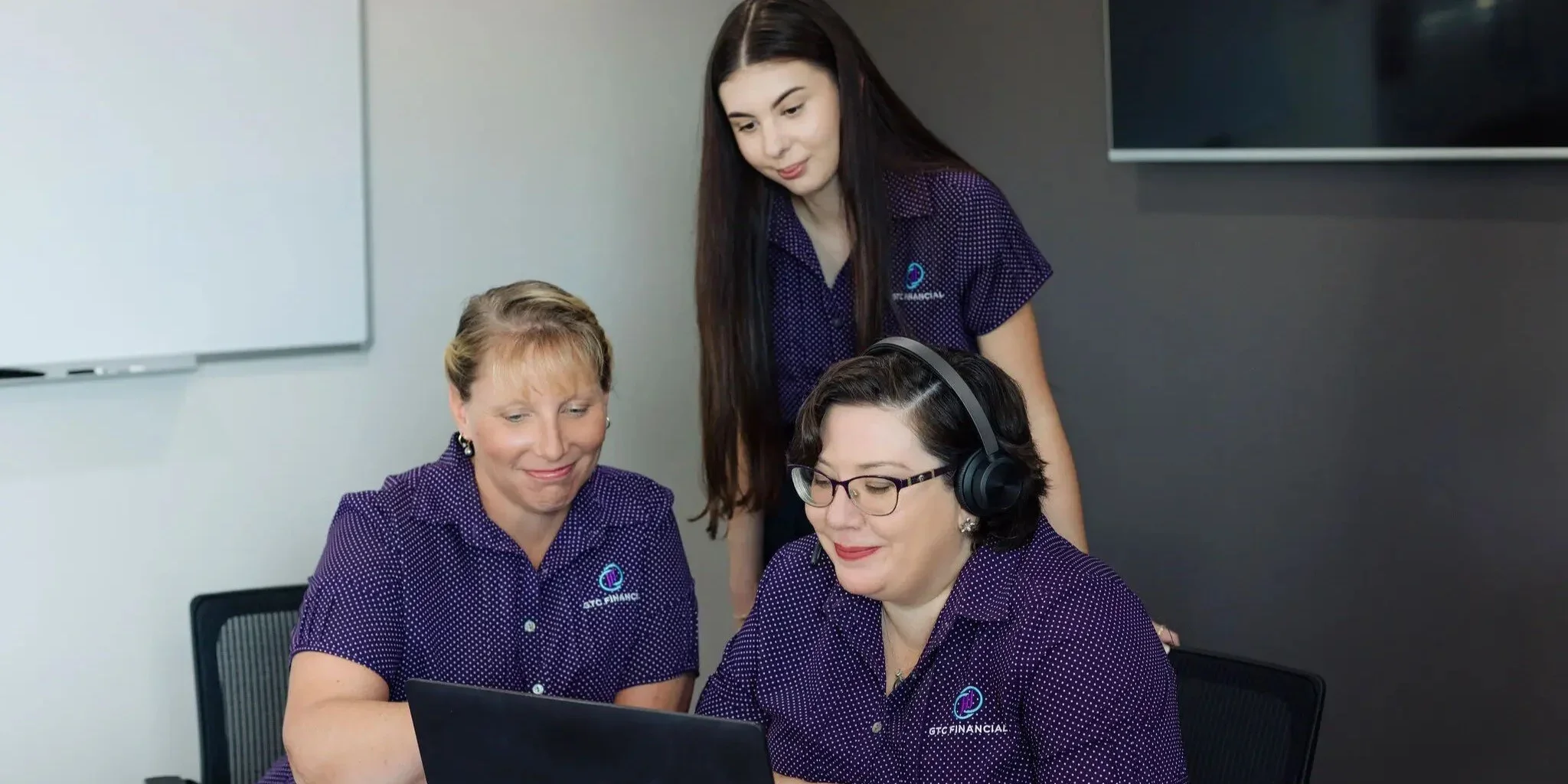

We’ve got the numbers covered,

so you can focus on what you do best

Ready to strengthen your business finances?

Let’s talk about your business goals. Book a consultation with our Gladstone team.